Abstract

The Monte Carlo method is a numerical approach for solving problems using random sampling. The original motivation for the method was to facilitate the resolution of partial differential equations appearing in natural studies, but has been adopted for the general solution of problems where an analytical solution is not available or too complicated to be used. Typical situations include optimisation, numeric integration, sampling from probability distributions, and random variable computations. This article discusses the fundamental elements of the method and provides guidance for implementation using standard spreadsheet software.

Random variables

A discrete random variable

The values

The expected value

The expected value has the following properties, where

The variance

The variance has the following properties, where

If a random variable

The following relationships are valid for independent random variables

A continuous random variable is defined over a continuous interval

generally

Two useful random variables

The random variable

It can be verified that

The random variable

It can be verified that

The Central Limit Theorem

A set of

Lets call the sum of these values

It can be seen that

Lets consider now a normal random variable

The central limit theorem states that for any interval

The central limit theorem is also valid for any sum of random variables (not necessarily identical and independent) provided that no single variable plays a significant role in the sum.

The Monte Carlo method

To determine some unknown value

Lets consider

Rearranging this equation we arrive at the Monte Carlo formula

![\Pr \left[ \left| \displaystyle\frac{1}{N} \sum\limits_{i=1}^N \xi_i - m \right| < \displaystyle\frac{3b}{\sqrt{N}}\right] \approx 0.997](https://s0.wp.com/latex.php?latex=%5CPr+%5Cleft%5B+%5Cleft%7C+%5Cdisplaystyle%5Cfrac%7B1%7D%7BN%7D+%5Csum%5Climits_%7Bi%3D1%7D%5EN+%5Cxi_i+-+m+%5Cright%7C+%3C+%5Cdisplaystyle%5Cfrac%7B3b%7D%7B%5Csqrt%7BN%7D%7D%5Cright%5D+%5Capprox+0.997&bg=ffffff&fg=000&s=0&c=20201002)

From this expression we can determine the expected value of the random variable

The method consists of sampling

Practical implementation

There are a number of commercial packages that run Monte Carlo simulation, however a basic spreadsheet program can be used in most situations. The generation of multiple trials is implemented by propagating a basic formula

A typical problem consists in the determination of an unknown value

Lets assume that the total cost of a project is the sum of the cost of a number of independent activities

An important assumption is that each of the variables is independent of the others. This means that the cost of any activity is not influenced by the cost of any other activity.

The general scheme of the Monte Carlo method is as follows:

- Generate random values for each of the activity costs

- Add these variables in a total project cost

- Repeat this operation

- The expected project cost is the average of the total project cost

The first step is to generate random values for each of the activity costs. Assuming a uniform distribution, we can use the RAND() function to generate random numbers in the interval (0,1) and multiply these by the range of each variable. The range is the difference between the maximum value and the minimum value

The cost for Activity

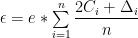

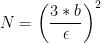

To determine the number of iterations we estimate the standard deviation

We can estimate an upper bound of

Note that we used the function STDEV.P, which calculates the standard deviation of the entire population, in this case only 3 values.

To calculate

The number of iterations to obtain a result with an error of less than

The kurtosis and skewness of the generated distribution will be close to the normal distribution.

Conditional variables

An important assumption is that the random variables are independent. Covariance is defined as:

![\sigma(\xi,\eta) = \textbf{E}[(\xi-\textbf{E}\xi)(\eta - \textbf{E}\eta)]](https://s0.wp.com/latex.php?latex=%5Csigma%28%5Cxi%2C%5Ceta%29+%3D+%5Ctextbf%7BE%7D%5B%28%5Cxi-%5Ctextbf%7BE%7D%5Cxi%29%28%5Ceta+-+%5Ctextbf%7BE%7D%5Ceta%29%5D&bg=ffffff&fg=000&s=0&c=20201002)

If

If the simulation model requires conditional random variables then they can be generated using the following algorithm:

- Generate two uniform random variables

and

- Generate a third random variable

Where

Variance Reduction Techniques

The Monte Carlo method produces a result that is the expected value

Common Random Numbers. If we are comparing two different systems it is better to use the same set of random numbers for both simulation runs. The idea is based on the following property of the variance:

If

Antithetic Variables. If

Therefore if

References

Metropolis, N; Ulam, S (1949) “The Monte Carlo Method”, Journal of the American Statistical Association, No 247, Vol 44